Overview

Following an 86-seat Labour Party majority, leading data and analytics company GlobalData expects the UK construction industry to contract in real terms by approximately 3% in 2024 and 1% in 2025.

Thereafter, rebounding conditional to forthcoming elections, high material costs, expanding foreign trade agreements, and tightening migration policy.

Go deeper with GlobalData

In turn, sidelining housing while presenting lucrative opportunities for energy construction stakeholders domestically.

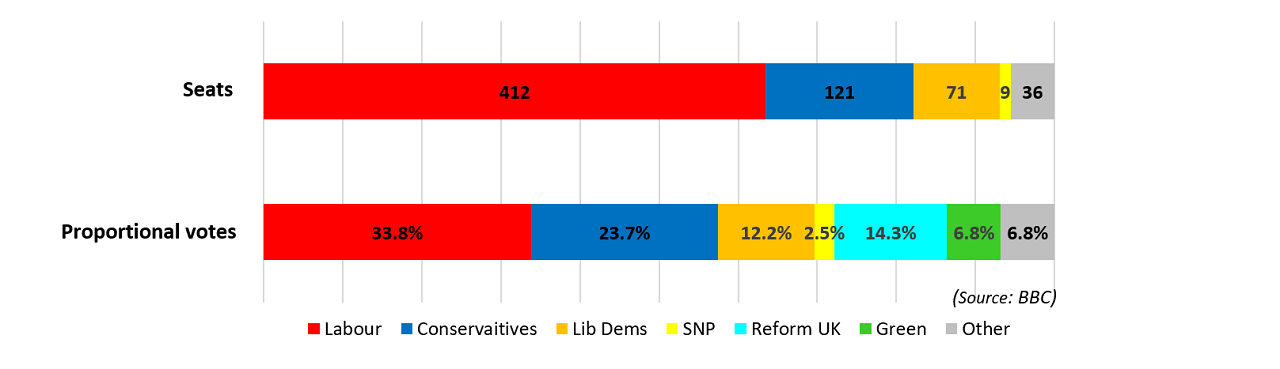

2024 UK election breakdown

On 4 July 2024, Labour seized 412 seats, surpassing the minimum 326 seats majority.

The Conservatives lost 240 seats, setting a precedent by losing 11 cabinet ministers in the party’s worst performance in history.

And despite limited seating (four seats acquired), Reform UK – formerly the Brexit Party – collected more than four million votes, 14.3% of total voting.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataAccording to Organisation for Economic Co-operation and Development data, under a Conservative government, 14 years of burgeoning house prices, inconsistent inflation, and unstable migration has seen consumer confidence fall from 101.07 in 2010 to 99.24 in 2024; this is uncoincidental to housing output falling short of targets set by the UK’s Department for Levelling Up, Housing and Communities Committee year-on-year (YoY) since 2020, Brexit, Covid-19, and fractured global supply chains consequent of evolving conflicts in Europe and the Middle East.

Moreover, settling interest rates – at 4.6% – did little to ameliorate weak Conservative polling as the Bank of England stresses autonomy in contradiction to Conservative fiscal policy.

Resultantly, Labour’s leader Kier Starmer has swung political favour, though approximately 80% of the UK population abstained/rejected voting for Labour, indicative of the challenge the government faces.

Pledges

Labour’s manifesto outlines plans to kickstart the UK’s construction output through its residential, energy, and utilities sectors.

Specifically, by 2028, investing £8.3bn ($10.62bn) to invent Great British Energy and £6.6bn to implement new Warm Home Plans; by 2029, developing 1.5 million new residential homes; and by 2030, ‘doubling onshore wind, tripling solar power, and quadrupling offshore wind’.

Furthermore, in pursuit of energy autonomy, Labour vows to fast-track construction for 5G infrastructure, nuclear labs, and battery manufacturing.

Resultantly, GlobalData expects energy and utilities construction to grow by an average annual growth rate of 4.17% between 2024 and 2028.

Whereas residential output is expected to contract by 3.4% in 2024 and 5% in 2025, subject to an exhausted government budget, high construction material costs, and labour uncertainty.

Despite stark differences between Labour and right-wing ideology, energy nationalisation policies align in popularity.

Caveats

First, high material costs handicap new project viability.

Despite the UK Department of Business, Energy, and Industrial Strategy‘s average construction material price index falling by 1.9% in the first three months of 2024, material prices remain high following increases in 2021 (15.2%), 2022 (19%), and 2023 (0.9%).

Markedly, pipes and fittings (22.3%), doors and windows (18.2%), and ready-mixed concrete (13.4%) rose respectively in 2023; all critical to residential building.

Hence, the total value of new construction orders awarded at current prices fell by 1.3% YoY in the first quarter (Q1) of 2024 following YoY declines of 27.8% in Q4 and 15.2% in Q3 2023.

In annual terms, the total value of new orders fell by 16% in 2023, decreasing from £80.8bn in 2022 to £67.9bn

Furthermore – in rebuke to Conservative fiscal policy – Starmer has been vocal about respecting limits set by the UK Office for Budget Responsibility while maintaining tax rates and ‘solving’ the budget deficit that as of May this year sits at £121bn, equivalent to 4.4% of gross domestic product.

Therefore, GlobalData speculates that a Labour government will be straightjacketed into prioritising energy over housing given the scale of its construction policies is beyond current fiscal capabilities.

Second, labour supply uncertainty hinders project planning and feasibility.

Proceeding net immigration surpassing 685 million in 2023, Ipsos’ Issues Index reports immigration as a paramount election issue behind the country’s National Health Service and the economy.

The unanimity of political consensus to tighten immigration suggests a diminishing influx of labour in the shortcoming; whereby, as of 2022, non-UK workers account for approximately 10% of total employment within the UK construction industry.

However, at present, the scale and method of UK immigration tightening is equivocal due to Labour campaigning vaguely conscious of its superior majority.

Furthermore, in the aftermath of Brexit, the UK Department of Business and Trade has set elusive targets to expand free trade agreements (FTAs) with India, Vietnam, Mexico, Turkey, Samoa, Fiji, North Macedonia, Morocco and Norway, having recently negotiated into the Comprehensive and Progressive Agreement for Trans-Pacific Partnership in July of 2023.

These FTAs pose prosperous to rebounding UK construction output but depend on the ability of Labour to negotiate material prices successfully whilst setting clear boundaries for migration flow domestically.

Final Remarks

Dwindling consumer confidence following 14 years of a Conservative government means Labour has won an 86-seat majority.

Starmer posits growth for the UK construction industry by focusing on the residential, energy, and utilities sectors, including nationalising energy through establishing Great British Energy.

Yet, project feasibility is handicapped by high material costs and labour uncertainty.

Resultantly, GlobalData expects the UK construction industry to contract in real terms by approximately 3% in 2024 and 1% in 2025, but expanding bilateral FTAs present a remedy to rebound output from 2026.

Nevertheless, the immediate, stunted output in UK construction will be defined by discrepancies between overzealous political promises and fiscal realities.